This article provides an overview of the global aerospace supply chain, examines the current state and potential of the Vietnamese market, and analyzes the opportunities and prerequisite conditions for small and medium-sized mechanical engineering enterprises to progressively integrate into the global aerospace value chain.

Amid the global aviation industry’s ongoing recovery and expansion, and as major manufacturers increasingly diversify their supply networks and seek new suppliers in emerging markets, the current landscape presents tangible opportunities for Vietnamese mechanical engineering enterprises to gradually integrate into appropriate segments of the aerospace supply chain. However, aerospace is a highly specialized industry characterized by stringent standards, rigorous processes, and strict production discipline. As such, participation requires a long-term, capability-driven approach grounded in demonstrable technical competence and sustained commitment. This article provides an overview of the global aerospace supply chain, examines the current state and potential of the Vietnamese market, and analyzes the opportunities and prerequisite conditions for small and medium-sized mechanical engineering enterprises to progressively integrate into the global aerospace value chain.

The Global Aerospace Supply Chain: Scale, Structure, and Industry Leaders

In an increasingly globalized economy, the aerospace industry is not only a symbol of international integration but also one of the most complex supply chains in modern manufacturing. Spanning raw materials, precision machining, system assembly, engine production, and maintenance, repair, and overhaul (MRO), the aerospace supply chain forms a vast ecosystem connecting hundreds of thousands of enterprises across multiple tiers worldwide.

- Market Size and Growth Outlook

Following the downturn caused by the pandemic, global air transport activity and aircraft production have shown clear signs of recovery, driving renewed demand for components, maintenance services, and engineering capabilities - ushering in a new growth phase for the aerospace supply chain.

At the level of complete aircraft manufacturing, the global commercial aviation market is estimated to reach approximately USD 415 billion in 2025 and is projected to grow to around USD 529 billion by 2030. However, when viewed across the broader supply chain - including components, modules, spare parts, and lifecycle replacement activities - the total economic value generated by the industry is significantly larger. The global aircraft parts and components market alone was valued at over USD 674 billion in 2023 and is expected to exceed USD 1.09 trillion by 2033, with an average annual growth rate of approximately 5%.

Beyond manufacturing, the MRO segment is also expanding rapidly. As the global fleet continues to grow, demand for scheduled maintenance increases accordingly, prompting operators and service providers to expand capacity while gradually shifting part of their operations to emerging markets, particularly in the Asia-Pacific region.

- The Multi-Tiered Structure of the Aerospace Supply Chain

The aerospace supply chain is characterized by a clearly tiered structure and a high degree of specialization, covering the full lifecycle from design and manufacturing to assembly, operation, maintenance, and technical support.

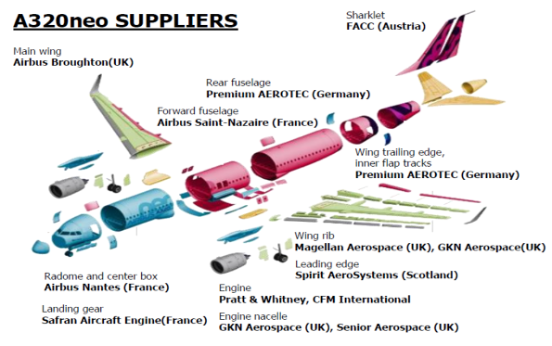

At the top tier are original equipment manufacturers (OEMs), with Airbus and Boeing serving as the two emblematic leaders in commercial aircraft production. These companies act as system integrators, responsible for overall design, program management, and final product accountability.

Below them are Tier-1 suppliers, including major corporations specializing in engines, airframes, landing gear, flight control systems, cabin interiors, and avionics - such as GE Aerospace, Rolls-Royce, Pratt & Whitney, Safran, and Collins Aerospace. These players possess strong R&D capabilities, manage extensive supplier networks, and form the backbone of the industry.

Tier-2 and Tier-3 suppliers focus on manufacturing structural components, mechanical parts, subassemblies, and semi-finished products. Their activities range from aluminum and titanium machining to surface treatment, heat treatment, jig and fixture fabrication, and tooling. While the number of companies at these tiers is significantly larger, the requirements for quality standards, traceability, and process discipline remain extremely stringent, as every component directly impacts flight safety.

At the foundation of the supply chain lies Tier-4, comprising providers of raw materials and essential technical services, including aerospace-grade aluminum and titanium, composite materials, surface treatment chemicals, testing and measurement services, and specialized logistics. Although less visible in aircraft programs, Tier-4 suppliers play a critical role in ensuring stable, standards-compliant inputs, forming the bedrock upon which the entire supply chain operates reliably.

Parallel to the manufacturing supply chain is the MRO service ecosystem, encompassing scheduled maintenance, component repair, engine overhaul, non-destructive testing (NDT), surface treatment, and spare parts logistics. This segment holds strategic importance, as it directly determines aircraft availability and operational cost efficiency for airlines.

In essence, the aerospace supply chain is a highly structured and interdependent network, where each enterprise contributes a specialized link, bound together by rigorous adherence to global technical standards.

- Global Hubs and Leading Players in the Aerospace Supply Chain

Today, North America and Europe remain the traditional centers of the aerospace industry, hosting the majority of OEMs, Tier-1 suppliers, and major research institutions. However, the ongoing shift of manufacturing and MRO capabilities toward the Asia-Pacific region is becoming increasingly evident, driven by cost advantages, a young and technically skilled workforce, and rapidly growing market demand.

Beyond Airbus and Boeing, several corporations serve as key driving forces within the global aerospace supply chain, including:

- GE Aerospace, Rolls-Royce, Pratt & Whitney, and Safran in aircraft engine manufacturing;

- Collins Aerospace, Honeywell, and Thales in avionics systems and cabin interiors;

- Lufthansa Technik, ST Engineering, and SR Technics in the global MRO sector.

These companies not only manufacture critical systems and components but also play a pivotal role in shaping technical standards, quality processes, and collaboration models across the supply chain. Participation in their networks—at any tier—requires suppliers to meet stringent requirements in safety, traceability, risk management, and the ability to maintain consistent, long-term production performance.

Vietnam’s Aerospace Supply Chain: Current Landscape and Level of Participation

Compared to countries with long-established aerospace industries, Vietnam is still at an early stage, gradually building its capabilities to participate in the global aerospace supply chain. Domestic activities are currently concentrated in areas such as aviation operations, basic MRO services, precision mechanical machining, and the production of a limited range of components. Meanwhile, higher-tier segments - including complex systems, advanced structural components, and design and R&D - remain in their nascent stages of development.

- MRO and Operational Technical Services

In 2022, Vietnam’s MRO market demand was estimated at approximately USD 654 million, while domestic capabilities were able to meet only around USD 151 million of that demand, with the remainder outsourced to foreign service providers.

Within the MRO segment, Vietnam currently has several key players, including VAECO (Vietnam Airlines Engineering Company), Vietstar Aero Engineering (VSAE), AESC - Aerospace Engineering Services JSC, and SAAM/SAMCO. These organizations primarily handle routine maintenance, partial repairs, and technical support services for domestic fleet operations.

However, existing capabilities remain concentrated at intermediate maintenance levels. High-value and complex overhaul activities are still largely carried out at regional MRO hubs such as Singapore and Malaysia. This underscores a key reality: while Vietnam’s MRO market demand is substantial, domestic capacity currently meets only a portion of it, leaving significant room for future development.

- Precision Machining and Component Manufacturing

In the segment of component manufacturing and precision engineering, the market currently sees participation from both domestic and foreign-invested enterprises. Notable players include Viettel Manufacturing Corporation (VMC), UAC Vietnam, and Hanwha Aerospace Vietnam. These companies are involved in machining structural components, aluminum and titanium parts, as well as producing tooling and jigs for selected orders within the international aerospace supply chain.

However, the number of enterprises that have obtained industry-specific certifications such as AS9100 or Nadcap remains limited. As a result, participation is largely confined to satellite roles or contract-based manufacturing for individual orders, rather than evolving into multi-tier supplier positions as seen in more mature markets.

- Logistics, Spare Parts, and Supply Chain Support Services

In addition to manufacturing and MRO, Vietnam’s domestic aerospace supply chain ecosystem also includes enterprises providing logistics and supporting services. Key players such as ALS (Aviation Logistics), SCSC Cargo, TCS - Tan Son Nhat Cargo Services, and Yusen Logistics Vietnam offer specialized spare parts warehousing, dedicated logistics solutions, AOG (Aircraft on Ground) handling, and cross-border transportation for aerospace components and equipment.

These companies play an important role in strengthening the operational and distribution links within the supply chain. However, the level of integration among domestic suppliers remains relatively fragmented, with limited development of a multi-tier, fully integrated value chain comparable to established regional aerospace hubs.

Overall, Vietnam’s aerospace supply chain has established an initial foundation, with the presence of several core players in MRO, component manufacturing, and technical logistics. Nevertheless, the level of participation by Vietnamese enterprises in the global supply chain remains modest, largely concentrated in selected segments rather than forming a comprehensive, multi-tiered ecosystem at scale. This represents both a current limitation and a significant opportunity for the industry’s next phase of development.

Opportunities for Vietnamese Mechanical SMEs: Building Fundamental Capabilities

As the global aerospace supply chain continues to evolve and the demand for new suppliers rises, the opportunities for Vietnamese mechanical engineering SMEs are both real and potentially significant. However, this is not a sector that can be entered through short-term approaches or opportunistic engagement. Instead, meaningful participation requires companies to build capabilities in a structured, strategic manner, underpinned by long-term commitment and sustained investment.

- What Opportunities Exist for Vietnamese Mechanical SMEs to Enter the Global Aerospace Supply Chain?

According to Mr. Nguyen Thanh Hoa, General Director of Makino Vietnam - part of Japan’s Makino Group, one of the world’s leading CNC machine tool manufacturers with strong capabilities in aerospace applications - the field of aerospace machining can broadly be divided into two primary product categories:

- Aircraft structural components (structure parts), typically machined from aluminum, characterized by large sizes and requiring high productivity and process stability.

- Engine components, which involve specialized materials such as titanium and heat-resistant alloys, and demand significantly more stringent technical standards and process controls.

These two segments exhibit distinct technical characteristics. Aluminum structural parts may not require ultra-high precision but do demand consistent machining stability and high throughput. In contrast, engine components impose far stricter requirements in terms of material properties, thermal resistance, and manufacturing processes.

As emphasized by Mr. Hoa, the aerospace industry requires exceptionally high levels of stability, precision, and production discipline. Delivery schedules allow virtually no deviation; many components must be processed using machines specifically optimized for particular materials and geometries to ensure consistent quality; and to mitigate the risk of production downtime, manufacturers often need to invest in at least two machines for the same operation. These requirements highlight that international partners prioritize not only cost competitiveness or short-term machining capability, but also the long-term reliability of the entire production system.

Mr. Hoa further noted that the global aerospace supply chain has been established and refined over more than a century of industry development. Over this period, companies have become deeply specialized across segments - from engines and structures to components and systems - while building strong in-house R&D capabilities and close collaboration with OEMs such as Airbus and Boeing on specific aircraft programs. As a result, supply chain relationships have been rigorously validated over time in terms of quality, reliability, and partnership stability. Replacing Tier-1 or Tier-2 suppliers is therefore highly challenging, as even OEMs are reluctant to assume the risks associated with shifting from long-standing partners to new, unproven suppliers.

Nevertheless, opportunities do exist - particularly in the lower tiers of the supply chain, where Tier-1 and Tier-2 companies actively seek additional satellite suppliers in emerging markets. Many global Tier-1 and Tier-2 players have already begun exploring Vietnam as a sourcing destination, especially in segments such as structural component machining, mechanical parts, and specialized components.

At the same time, geopolitical shifts, supply chain diversification strategies, and the rapid growth of the regional aviation market have prompted international corporations to seek alternative manufacturing bases beyond China. In this context, Vietnam is increasingly viewed as a promising option, supported by its developing industrial infrastructure, technically capable workforce, and competitive cost advantages.

- The Biggest Barrier: Mindset and Long-Term Commitment

Many domestic enterprises tend to view technical standards, certifications, specialized equipment, or initial investment costs as the primary barriers to entering the aerospace sector. However, according to Mr. Do The Dang (Aerospace Network / AESC), the more fundamental question lies in mindset and strategic commitment. In his view, the key question for Vietnamese enterprises is not “Can we do it?” but rather “Do we truly want to do it?”

Once a company commits to entering the aerospace industry, it must be prepared to invest comprehensively in people, processes, machinery, standards, and international certifications - rather than approaching the sector through short-term or opportunistic efforts.

One of Vietnam’s pioneering cases in accessing the global aerospace supply chain is Viettel Manufacturing Corporation (VMC). According to Mr. Luu Chi Cuong, Business Development Director of VMC’s Aerospace Center, the company began implementing the AS9100 quality management system - the aerospace industry’s standard - at an early stage and achieved certification in 2019. Building on this foundation, VMC continued to upgrade its manufacturing capabilities to meet special process requirements and subsequently attained Nadcap certification for post-machining surface treatment.

Mr. Cuong emphasized that achieving AS9100 is not an unattainable goal. For companies already experienced in precision manufacturing for industries such as automotive and motorcycles, the standardization process can take as little as one year - provided there is strong commitment and proper implementation.

However, beyond equipment and technology, VMC places particular emphasis on traceability discipline and detailed process control, which are critical requirements in the aerospace sector. Every component, material batch, and production step must be fully traceable. This ensures that even the smallest deviation can be quickly identified, risks can be contained, and preventive measures can be implemented to avoid recurrence. This level of system reliability is often valued more highly by international partners than cost competitiveness or standalone technical capability.

By adopting a structured, phased approach - from team building, technology research, and prototyping, to small-scale production and gradual capacity expansion - VMC has progressively strengthened its collaboration with global Tier-1 contractors. This case demonstrates that participation in the global aerospace supply chain is not an overly risky endeavor, but rather a feasible path for companies willing to invest systematically in standards, systems, and human capital.

Overall, opportunities for Vietnamese mechanical enterprises to enter the global aerospace supply chain are tangible, but they do not lie in short-term or fragmented approaches. This is a long-term journey that requires sustained investment in people, standards, processes, and operational capabilities, alongside careful selection of segments aligned with each company’s current capabilities and development trajectory. Early success stories show that with the right approach and long-term commitment, Vietnamese enterprises can gradually establish their position within suitable segments of the aerospace value chain.

In this context, the role of intermediary organizations and industry associations is becoming increasingly important. The Vietnam Association for Supporting Industries (VASI) has initiated efforts to support member companies in accessing the aerospace supply chain - through information sharing, standard orientation, and fostering collaboration with both domestic and international partners. If implemented in parallel with strong commitment from enterprises themselves, such initiatives could serve as a critical foundation for Vietnam’s mechanical engineering sector to move further into high-value, technology-intensive global supply chains in the future.